Back in April I wrote a blog post titled Portfolio Management Decision-Making that highlighted the difficulty in developing an effective risk-managed portfolio of investments to meet client goals. On the one hand, it could be a very simplistic approach with just two holdings: the S&P 500 for the equity piece and the Bloomberg U.S Aggregate Bond Index for the fixed income piece. But, we all know that the investment universe is much more complex than that and is made up of a multitude of different sectors and sub-sectors.

Many investment managers provide “model” investment portfolios that attempt to target risk profiles by adjusting the sector and sub-sector weightings of equities and fixed income. A typical model portfolio can be comprised of 60% equities and 40% fixed income with some diversifying allocations to other sub-sectors.

The main difference between any of these models is the allocation to the equity and fixed income sub-sectors. The equity sub-sectors most often seen are small- and mid-cap equities, international developed and emerging market equities, and growth or value style. In the fixed income space it is common to see high yield bonds, corporate bonds, and emerging market bond sectors. Needless to say, the allocations to the sub-sectors are the factor most driving investment performance.

I took a look at a few of the large investment model providers: State Street, Vanguard, and WisdomTree (see table below). They each provide long-term strategic model portfolios comprised of equity and fixed income sectors. I analyzed two specific strategies: the 60% equity / 40% fixed income growth strategy and the 80% equity / 20% fixed income aggressive strategy.

As seen below, none of the models consistently beat their naïve benchmarks (iShares Core Growth for the 60%/40% strategy and iShares Core Aggressive for the 80%/20%). Though all of the models target the overall equity/fixed income allocation, it is the underlying sector allocation that drives the difference. In these cases, sometimes they win (green highlight) and sometimes they lose (no highlight)!

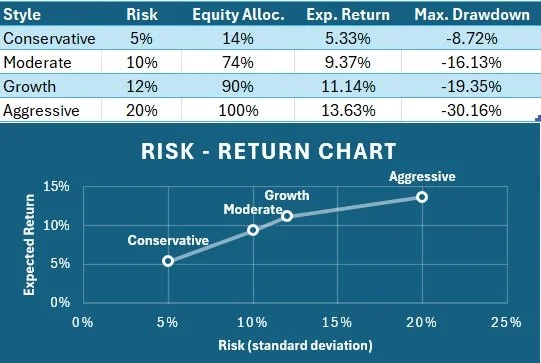

D&A model portfolios are most usually customized for each client depending upon their specific unique preferences. Model portfolios offer frameworks, but customization is key to achieving client goals. Most accounts are made up of some core holdings in the S&P 500 and Core bonds, but most usually over 50% is allocated to diversifying positions. Also, some weighting is often given to thematic or other positions in the investment factor, technology, or other sub-sector.

As I said in that April blog post,

There are literally an infinite number of combinations of equities and fixed income to create a portfolio with similar levels of risk, so SOMEONE needs to make an investment decision and invest in SOMETHING! That is my job, as an investment adviser, to use my experience and knowledge of the markets to understand client objectives and goals to create an appropriate diversified portfolio with a target level of risk.