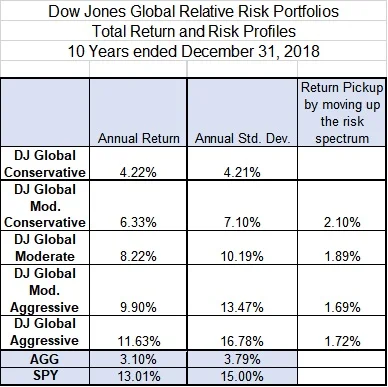

Long term strategic investing is usually baselined against naïve mixes of the S&P 500, as a proxy for a broad mix of large cap U.S. stocks, and the Bloomberg Barclays U.S. Aggregate Bond Index (AGG), as a proxy for broad core bonds including U.S. government and investment grade corporate bonds. These broad naïve categories, however, miss many areas of the capital markets and optimized asset weighting that could provide extra diversification and additional return per unit of risk.

So far during 2019, some of the passive exchange-traded funds (ETFs) that are designed to track a broader selection and optimized mix of assets have added incremental return to naïve mixes of the S&P 500 and AGG.

Two equity ETFs that have done well are the iShares Edge MSCI Min Vol USA (USMV) and the iShares Edge MSCI USA Momentum Factor (MTUM). Both of these ETFs are structured to capture some of the “factor” anomalies that research has shown to outperform the naïve S&P over time. YTD through May 24, USMV and MTUM have returned 14.93% and 14.06%, respectively, whereas the S&P 500 (SPY) has returned 13.64%.

Real estate investment trusts (REITs) are a good asset class to help diversify equity exposures and also hedge against inflation. An ETF that tracks that asset class is the Schwab US REIT ETF (SCHH). Real Estate Investment Trusts tend to be a more risky subset of the equity space and has returned 17.26% so far in 2019, beating the 13.64% of the S&P 500.

Another innovative ETF that helps diversify exposure is the AI Powered Equity ETF (AIEQ). This ETF uses artificial intelligence in the portfolio management process with a target to outperform the S&P 500 with a similar amount of risk. Year-to-date through May 24 this ETF has returned 17.74%, easily outpacing the 13.64% of SPY.

Likewise, selected carveouts of the fixed income space have easily beat the Bloomberg Barclay Aggregate U.S. Bond index (AGG). While the AGG has returned 3.76% YTD, other fixed income sub classes have added incremental return and diversified exposures. For example, preferred stocks (represented by iShares Preferred & Income Securities ETF, PFF) has returned 9.03%. Additionally, the high yield bond, investment grade corporate bond, emerging market bonds, and bank loans (tracked by HYG, LQD, EMB, and BKLN) have all outperformed AGG with 7.49%, 7.42%, 7.10%, and 6.44% respectively, against the AGG of 3.76%.

In this environment, a broader diversification approach and optimized weighting will help portfolios to outperform the naïve S&P 500 and the AGG.